Proxima Fusion has raised a 411 million euro Series A, among the largest early rounds in European deep tech, to pursue a stellarator approach to fusion power. Counting grants and prior funding, the Munich company has now pulled in more than 650 million euro, with a backer list that spans XTX Ventures, Google and the German utility RWE. The reason this is notable beyond the headline number: Proxima is betting on the stellarator, the harder-to-build but inherently steadier cousin of the more common tokamak, and it is doing it from Europe rather than the US or China. Our take is that fusion has quietly become a fundable category, and the winners will be decided by engineering execution, not physics debates.

- Proxima Fusion closed a 411 million euro Series A, one of Europe's biggest, for stellarator fusion.

- Total funding now exceeds 650 million euro including grants; backers include XTX Ventures, Google and RWE.

- Stellarators are harder to engineer than tokamaks but run in a steadier state, avoiding some instabilities.

- The round signals investor appetite for European deep tech and for fusion as a fundable, not just academic, bet.

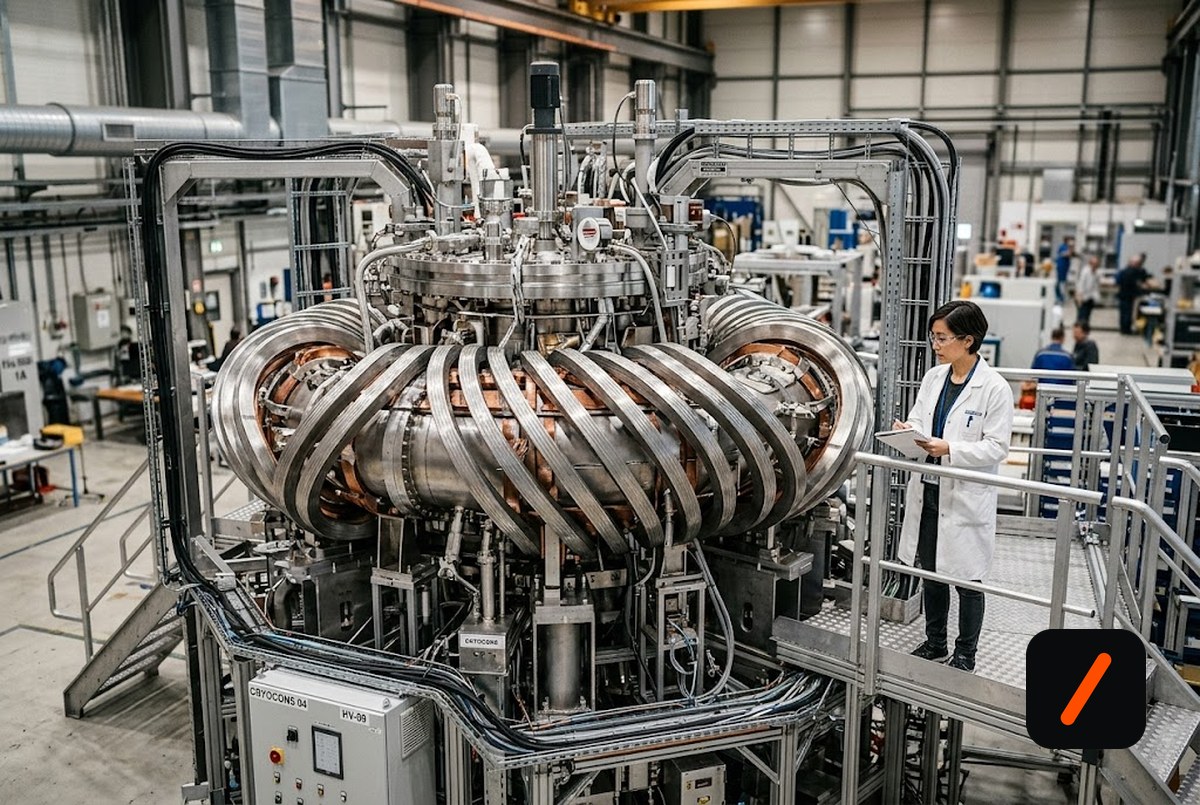

What is a stellarator, and why choose the hard path?

Both stellarators and tokamaks confine superheated plasma with magnetic fields, but they get there differently. A tokamak uses a simple donut shape and drives a current through the plasma to hold it, which works well but tends to pulse and suffers disruptions. A stellarator twists its magnets into a fiendishly complex geometry that confines the plasma continuously, without that internal current. It is far harder to design and build, which is exactly why modern simulation and precision manufacturing are what make Proxima's bet plausible now when it was not a decade ago.

RelatedMercury Raises $200M Series D at a $5.2B Valuation

Why is this round significant for Europe?

European deep tech has long complained that the biggest checks flow to Silicon Valley. A 411 million euro Series A into a hard-science company headquartered in Munich is a counterexample, and the presence of an industrial utility like RWE alongside financial and strategic investors signals that energy incumbents are treating fusion as a real supply-side option rather than a science-fair project. It also builds on Europe's genuine research heritage in stellarators, which gives Proxima a talent and knowledge base to draw on.

What does it mean for the valuation and the sector?

For investors the signal is that fusion has crossed from science funding into venture-scale capital, joining a cohort of well-funded private efforts. The read is not that grid power is imminent; it is that the risk profile now looks fundable, with milestone-based progress that capital can underwrite. Proxima remains private, so the exposure is through its strategic backers and the broader thesis that whoever demonstrates a workable reactor first captures an energy market measured in trillions. The savvy watch item is hardware milestones, a working magnet system and a demonstration device, not press releases.

Who benefits if it works?

Everyone downstream of electricity, eventually, but first the industrial supply chain: superconducting magnet makers, precision manufacturers, and the utilities that would site early plants. The nearer-term beneficiaries are the engineers and physicists a round this size can hire, and the European deep-tech ecosystem that gets a flagship to point at.

RelatedRunPod Raises $100M Series A for Its GPU Cloud

How does a fusion startup make money before power?

No fusion company is selling grid electricity yet, so the near-term business is milestones, not megawatts. Capital is deployed against a sequence of demonstrable technical achievements, a working magnet system, a plasma-confinement demonstration, a pilot device, each of which de-risks the next raise and, ideally, produces intellectual property and hardware capability that has value even if commercial fusion arrives later than hoped. Proxima's stellarator focus leans heavily on advanced superconducting magnets and precision manufacturing, and those competencies transfer: the same magnet and simulation expertise underpins medical imaging, particle physics, and grid infrastructure. That is part of why strategic investors like a utility are at the table, they are buying optionality on an energy source and a first look at the supply chain that would build it.

Is Europe actually competitive here?

On stellarators specifically, yes. Europe has decades of research heritage in the design, most famously the large experimental device that proved the concept could confine plasma in a steady state. Proxima is commercializing that lineage with private capital rather than waiting on multi-government megaprojects. A 411 million euro round says investors believe the engineering, not just the physics, is now within reach. It also gives Europe a flagship private-sector fusion story to rally talent and follow-on capital around, at a moment when the biggest checks have historically crossed the Atlantic. Whether that momentum holds depends on hardware, but the capital is now here to build it.

- Magnet milestones. The stellarator stands or falls on its complex superconducting magnets; watch for a working demonstrator.

- Follow-on capital. A round this size needs a bigger one behind it; the next raise tests conviction.

- Utility involvement. RWE at the table hints at where a first plant could actually land.

- OfficialProxima Fusion company site and announcements company primary

- FundingGenZTech Funding Tracker round logged in our data

Original analysis by GenZTech. Primary source: Proxima Fusion.